One of the mainstays of the global order for the past seventy years has been American economic leadership and the use of the US dollar as the core means of exchange, store of value, and unit of account. This global function has never been without difficulties—in the aftermath of Bretton Woods and the Nixon Shock, scholars like Robert Triffin and Susan Strange identified the domestic and international costs of dollar dominance. The debate reignited after the global financial crisis of 2008, with some scholars warning that increased politicization of the dollar may prompt a gradual transition into a multipolar global currency system, and others continually championing the dollar’s institutional strength and the absence of credible alternatives.

Recent geopolitical conflicts around the world have only exacerbated doubts about the future of American hegemony, including the future of its currency. Unpredictable political leadership, trade wars, and the eruption of armed conflict in Europe and the Middle East have heralded a new era for the global system and generated proliferating predictions of de-dollarization. All this has accelerated in Trump’s second term, which seems to be actively laboring to throw the status of the dollar into disarray. The retreat from open markets, unpredictable fiscal policy, blustering confrontation with the Federal Reserve, and threats to reduce service on foreign holdings of US treasuries have all registered a significant departure from business as usual in Washington. An as yet speculative “Mar-a-Lago Accord,” devised by recent appointee to the Fed Board of Governors, Stephen Miran, sets forth an agenda to actively weaken the dollar in a bid to boost domestic manufacturing and reduce trade deficits. Though unlikely to come to fruition, its very articulation by those closest to the President stands as another threat to the credibility and reliability of the dollar.)“Principled and pragmatic: Canada’s path” Prime Minister Carney addresses the World Economic Forum Annual Meeting(<)/a(>),” by World Economic Forum, January 20, 2026).” class=”footnote” id=”footnote-1″ href=”#footnote-list-1″>1 And with US military interventions causing more havoc in the global economy, the latest of which has prompted Tehran to all but close the Strait of Hormuz, questions of a new petro yuan or the introduction of a BRICS currency are gaining steam.

The historical record suggests, however, that a transition away from the dollar will be no simple task. Over the course of the last two centuries, there has been only a single transition from one leading international currency to another. This occurred in the aftermath of the Second World War, when the US dollar overtook the pound sterling as the main currency for international trade and as the leading reserve asset for national central banks.

It was in the nineteenth century that sterling established its predominance as a unit of account, a store of value, and a means of exchange. It was able to do so because of the pound’s credible commitment to gold parity, the global reach of British trade and investment, the prowess of the financial services in the City of London, and, in a pinch, the saving graces of the French and Russian banking elite.

After the Second World War, the dominant position of the American economy and the relative fall of Britain as a global power in the context of decolonization sparked predictions of decline similar to those made on the dollar today. But on its own, British hegemonic decline was not sufficient to facilitate the global currency shift we observed in the mid-twentieth century. It took a concerted effort among the central banks of the leading industrialized countries to manage the retreat of sterling. An array of cross-border central-bank cooperation in the form of credits and swaps, combined with British guarantees of the dollar value of national central banks’ sterling reserves, allowed a more graceful and predictable drop in sterling’s share of global reserves during the 1960s.

As the dollar grew dominant as a means of exchange, its attractions as a store of value had to be supported by coordinated market intervention to sustain its gold price throughout most of the 1960s. A damaging tipping point between sterling and the dollar was only avoided by carefully orchestrated multilateral support in the context of a shared Cold War commitment to stabilizing the international monetary system.

Our current geopolitical juncture certainly exhibits signals of hegemonic decline resembling those of Britain in the mid-twentieth century. But these signals alone may not be enough to overturn a complex, layered, and truly global currency system that was carefully constructed over the course of decades. Where the leading central banks have cooperated since 2008, it has been to sustain access to the dollar in the form of swap lines with the US Federal Reserve. At the present moment, it is difficult to imagine the US actively supporting a currency transition in the way Britain did in the postwar period. Though cracks in the dollar system may be deepening, we ought to be conscious of the complexity and depth of the existing monetary order. Ultimately, we may find that the US’s currency proves more resilient than its claim to political hegemony.

A coordinated rise

While the rise of the dollar might seem inevitable in hindsight, it required nothing less than the reorganization of the world’s economy. In the 1940s, the international monetary system was designed at Bretton Woods with the dollar as the anchor for the pegged exchange-rate regime. This encouraged countries to hold dollar-denominated foreign exchange reserves at their central banks to protect the dollar value of their currencies.

British policy also promoted the shift. In 1957, the British Treasury introduced fresh exchange controls on the use of sterling for third-party trade finance to discourage the international commercial use of the pound. Along with controls on domestic interest rates payable on deposits in both the US and the UK, these new restrictions on the use of sterling encouraged banks in London to turn to the dollar as the main currency for international commercial and financial services.

The other main contenders, Germany and Japan, resisted foreign demands to use their national currencies while they focused on their domestic industrial strategies. New York’s capital markets grew quickly, but the international banking and foreign-exchange market in the City of London continued to lead the world, due in no small part to the influx of American and European financial institutions. By the 1960s, the Eurodollar market in London promoted the dollar as a cross-border means of exchange and unit of account, while the structure of the international monetary system established the dollar as the premier store of value for global reserves.

The global payments system, too, was transformed to accommodate the dollar’s international role. The growth of the offshore dollar market in London in the late 1960s had dramatically increased the volume of cross-border dollar payments, causing a bottleneck among the correspondent banks managing these payments in New York. In 1970, the New York Clearing House introduced a market-leading computerized clearing system for cross-border dollar payments. This was the Clearing House Interbank Payments System (CHIPS), which made dollar clearing and settlement much more efficient for banks around the world through their correspondent partner banks in New York. No other center had a similar system, and access was restricted to members of the New York Clearing House, privileging large American banks.

British banks considered setting up a similar dollar clearing facility in London in 1969, but they concluded that the benefits would mainly flow back to the big New York banks given the dominance of CHIPS, so the project was abandoned. The sterling equivalent of CHIPS, Clearing House Automated Payment System (CHAPS), was only introduced in 1984. Originally controlled by banks themselves, it was taken over by the Bank of England in 2017.

But creating a system for cross-border and cross-currency clearing and settlement proved much more challenging than global dollar clearing in New York. Legal and operational differences, as well as heightened settlement risk across markets and time zones, made it difficult to construct a unified system. The collapse of the mid-sized Herstatt Bank in 1974 demonstrated how the tangled skein of global payments could be interrupted. Herstatt Bank was closed by the German authorities while New York’s correspondent banks were still open, leaving many banks without the funds they had expected to reimburse them for payments they had already made on Herstatt’s instructions. This “Herstatt Risk” (settlement risk compounded by time zone) took over twenty years to resolve, while the volume of payments (and therefore the amount of funds at risk) increased dramatically.

The private banks step in

In 1977, a group of internationally active banks launched the SWIFT messaging system, providing computer-based messages between banks for payments. SWIFT gradually replaced the telex system, which was time-consuming and prone to error. Still, delays in settlement meant that banks were exposed to high levels of risk if a counterparty bank failed during the day of a transaction, or if the operating system malfunctioned. Trust in counterparties remained an important element in the free flow of funds around the world. The real challenge was to create a system that netted payments in and out continuously throughout the day on a global basis so that only the smaller net amount had to be settled. SWIFT helped streamline communications, but didn’t offer a solution to settlement risk.

Both CHIPS and SWIFT were designed and implemented by large international banks and served their interests as gatekeepers. For example, SWIFT services were extended to South America before Africa or the Middle East to suit the location of servers in the US. New members had to pay large fees to join and guarantee a minimum volume of message traffic, so banks and countries with a smaller amount of payment traffic were disadvantaged. South Africa was the only African country to be connected to SWIFT in the 1980s, despite anti-apartheid sanctions, which applied to trade but not payments. The fact that larger institutions in wealthier countries continue to benefit most from the payments architecture was wired into the way the systems were designed by banks themselves in the 1970s.

The design of the multilateral payments netting and settlement system was similarly left to the private sector. From the mid-1980s, competing groups of banks in Europe, the US, and Canada tried to develop schemes that would be robust across jurisdictions and resilient in the event of failure of one or more large members. In 1990, the central banks of the world’s wealthy industrialized countries set minimum standards for these schemes to try to ensure systemic resilience, but their efforts to urge banks to take seriously the risk of their cross-border foreign exchange exposures fell on deaf ears. It wasn’t until 1997 that the banks came together in a single scheme to form the Continuous Linked Settlement (CLS) System. It would take another five years to launch.

Importantly, CLS only processes payments in a limited number of currencies. This means that most of the world’s currencies are excluded from its risk mitigation features: for most, transactions still need to go through the US dollar or carry the settlement risk outside the system. Although the number of currencies used in CLS has more than doubled (eighteen currencies are now included) many are still excluded, including the renminbi (RMB). Access to CLS is also carefully controlled so that there are only seventy-six direct members out of the many thousands of internationally active banks around the world.

A currency at the crossroads

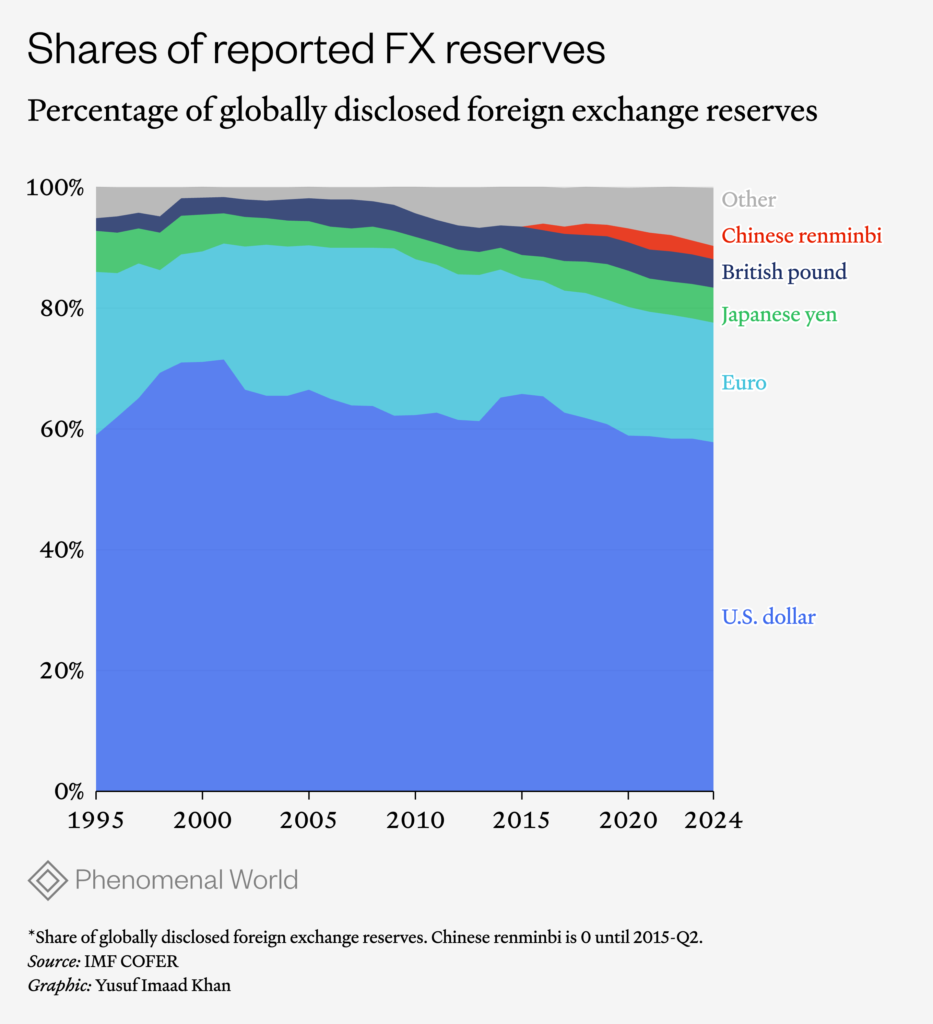

Has the world begun to drift away from the dollar? The currency’s international role is often measured by its share of global foreign exchange reserves. Figure 1 shows that the dollar’s share of recorded reserves currently sits near the 60 percent mark, where it has been for the past thirty years.

On this measure, it could be argued that we are already in a multipolar currency world and have been for decades. Central banks and treasuries around the world already manage diversified portfolios of assets, including gold, several national currencies, and even cryptocurrencies. While shifts in these portfolios could still be disruptive, we should be aware that our current, diversified system has proved stable for decades.

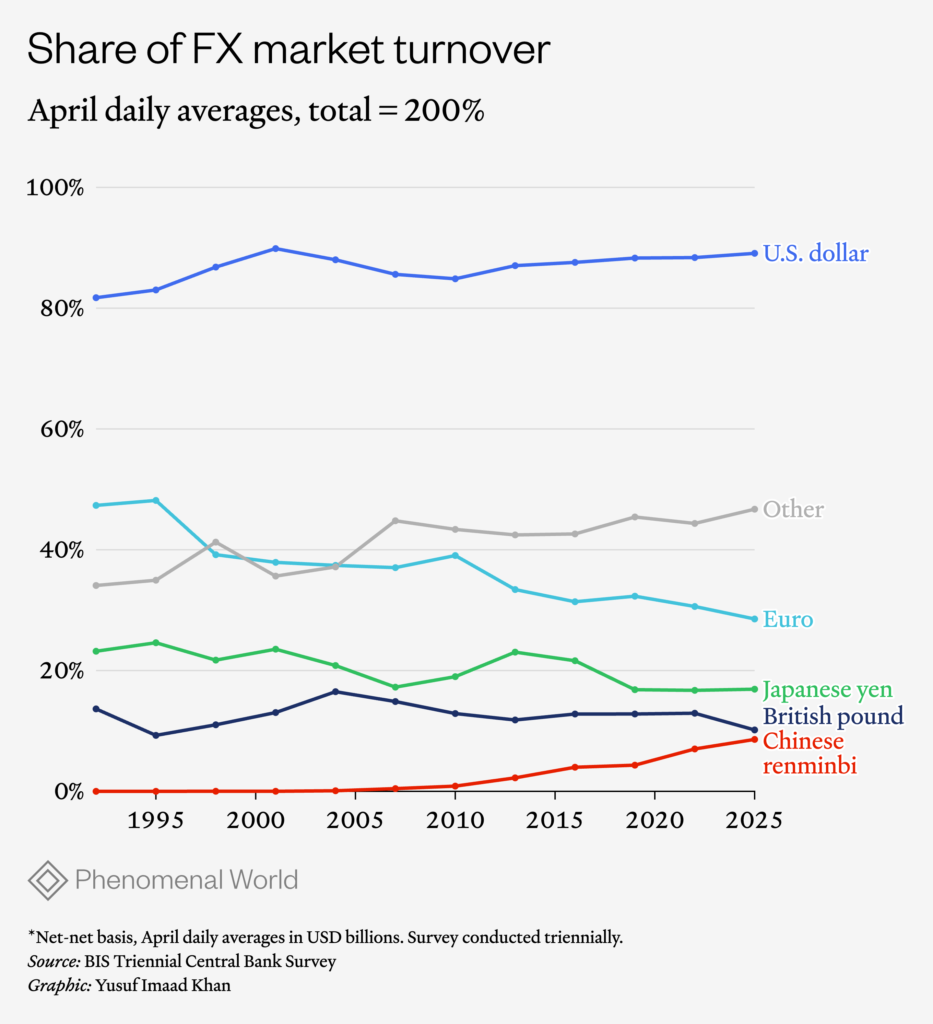

As a means of exchange, however, the dollar remains much more dominant. In each day of 2025, an average of $9.5 trillion worth of trades passed through foreign-exchange markets, 90 percent of which involved the US dollar on one side or the other of the trade. As is the case with the dollar as reserve currency, Figure 2 shows remarkable stability over the past thirty years, albeit with some decline in euro transactions, and a small increase in RMB, due partly to exchange-rate changes.

When it comes to its role as a means of exchange, there are two ways the dollar is used. First, it is commonly used as a unit of account in contracts, and therefore for settlement of financial and commercial payments. Second, the dollar is used as an intermediary step when converting two other currencies, where there may not be a liquid market in which to make a direct bilateral conversion. This vehicle currency role persists as an effect of the structure of markets.

The increased politicization of the dollar has appeared to threaten this stability. Iran has been a periodic target of repeated rounds of US financial sanctions since the 1970s. After the September 11 attacks, the US Treasury secretly issued subpoenas for data from SWIFT to track payments by suspected terrorists, a practice that was only revealed publicly in 2006, prompting a legal row with the European Union (EU), as SWIFT is headquartered in Brussels. This led SWIFT to open a server in Switzerland to offer its customers ways to avoid having their data stored in the US. In 2012, Iranian banks were disconnected from SWIFT, and in 2022, several banks from Russia and Belarus were similarly excluded to make it more costly for them to send and receive funds for their customers. Banks were forbidden from providing correspondent banking services for sanctioned entities, which prevented them from using the dollar, sterling or euro to settle commercial payments.

Such sanctions push transactions into more circuitous and expensive routes to avoid the use of the dollar or the currencies of other sanctioning political entities like the UK and the EU. The vulnerability to American sanctions has also led countries to create alternative payment systems, such as the China Interbank Payment System (CIPS), which was launched in 2015 to promote the international use of the RMB to settle trade. When Iran blocked shipping through the Strait of Hormuz in March, it seriously affected China’s trade, sparking rumors that Iran would make an exception for oil paid for in yuan. Along with the sanctions on payments for Russia’s oil, such a development could begin to break the dominance of pricing and settlement of the global oil trade in dollars. The more actors in a market that use a currency, the more useful it becomes. These forces also encourage convergence to a single or small number of key currencies.

But the politicization of the dollar is in itself nothing new. As early as 1951, at the very moment of the dollar’s ascendance, the US administration froze the dollar-denominated assets and payments of Chinese entities associated with the Chinese Communist Party. Because Britain did not restrict China’s use of sterling at the time, it then became more useful and prominent in China’s trade. While the use of sterling did increase as a result of these geopolitical tensions, it did not significantly alter the dollar’s overall status.

As was the case then, alternatives to the dollar remain marginal. Gold earns no interest and its supply is limited, the yuan remains partially behind capital controls, and the euro remains a money without a common fiscal policy. Deep and liquid financial markets are needed to support an international currency where holders want to be sure of their ability to move in and out quickly and cheaply. International currencies are indeed useful; traders want to use a currency that they know will be accepted by a wide range of counterparties. But without a more profound development of the global payments infrastructure, it is hard to increase use beyond a certain point.

In fact, the US payments infrastructure appears to be even more robust than before. International payments denominated in dollars are growing. Since sanctions were applied to payments to Russia, the share of SWIFT messages denominated in US dollars has increased from about 40 percent in the four years before 2022 (more than twice the share of the rival euro) to 58 percent in January 2026.)Innovative MyStandards technology from SWIFT fast tracks ISO 20022 onboarding(<)/a(>), February 2026. Data excludes intro-EU payments. The next most prominent currency is the euro, with about 14 percent of messages in January 2026.” class=”footnote” id=”footnote-10″ href=”#footnote-list-10″>10 Though China is among the world’s largest trading economies, the RMB is used for only a tiny amount—currently 3 percent—of cross-border payments. (As much as 75 percent of these are initiated by the special administrative region of Hong Kong, which falls under Chinese sovereignty.) Its own payments infrastructure, CIPS, relies on SWIFT. China has only recently begun developing its own messaging system in a bid to secure more independence from US systems. Though more foreign banks have been joining CIPS in recent years, the vast majority of members are Chinese banks and their subsidiaries around the world. This means that at present, the RMB payments infrastructure is not a serious competitor to the dollar-based one.

In 2009 and again in July 2025, the People’s Bank of China tried to overcome these barriers by promoting the use of the International Monetary Fund’s Special Drawing Right (SDR) as an alternative international currency. But the SDR, which was launched in 1969, and offers countries a right to draw on convertible currencies, is a complex instrument. Because their value is measured through a weighted basket of five currencies, it ultimately reflects political, rather than purely market-driven, calculations. The bureaucratic and fundamentally political nature of SDRs has stalled efforts to use them as an effective replacement to the dollar.

Cryptocurrencies might appear as another possible source of instability for the dollar, and there has been a surge in the use of stablecoins, especially for payments. They offer more anonymity to their users and don’t need to clear through New York. Tether, for example, is the most used stablecoin with the highest capitalization, but its value depends on backing by US dollar assets, linking it fundamentally to the dollar. In this way, the growth of stablecoins actually increases the demand for dollar assets and the indirect role of the dollar in international transactions rather than replacing the dollar per se. Efforts to build a workable cross-border system for central-bank digital currencies have struggled to overcome issues with interoperability and legal harmonization. mBridge is among the most advanced, gathering central banks of Hong Kong, China, Thailand, and the UAE, but it is still in the early stages of development.)reported(<)/a(>) to have been completed, amounting to the equivalent of $55 billion. The first direct government payment was made in November 2025 between the UAE and China.” class=”footnote” id=”footnote-12″ href=”#footnote-list-12″>12

Over the course of the last seventy years of crises and transformations in the global order, the dollar appears to have been resilient to the twists and turns of American policy, technological change, and geopolitical frictions. The currency distribution of global foreign exchange reserves and foreign-exchange markets has been remarkably stable for over thirty years and remains so even now, amid increasing political disorder. Even if the American empire itself is showing signs of fragmentation, the decline of the dollar is by no means assured. With no viable alternatives on the horizon, and in the absence of intense coordination among regional and global powers, the status of the US currency—and the global payments system that underpins it—may outlive expectations.

{kind=link}